Gard’s P&I (only) Combined ratio, including the 2016/17 reduction in deferred call, was 91%. Had the full estimated total call been made in 2016/17, the P&I combined ratio would have been 75%.

The Gard Group’s combined ratio for 2016/17, as the premium was actually charged, was 95%. Had the full estimated total call been made in 2016/17, the Gard Group combined ratio would have been 83%.

| Gard P&I only income and expenditure summary | 2014/15 | 2015/16 | 2016/17 |

|---|---|---|---|

| Income and Expenditure | |||

| Calls and Premiums | 628,672 | 607,260 | 531,601 |

| Reinsurance Premiums | -132,615 | -137,214 | -117,371 |

| Operating Expenses | -59,723 | -50,494 | -50,752 |

| Operating Income | 436,334 | 419,552 | 363,478 |

| Gross Paid Claims | 422,066 | 411,716 | 437,152 |

| Net Paid Claims | n/a | n/a | n/a |

| Net Change in Provision for Claims | n/a | n/a | n/a |

| Net Incurred Claims | 425,970 | 351,938 | 325,585 |

| Technical Surplus (Deficit) | 10,364 | 67,614 | 37,893 |

| Investment Income | n/a | n/a | n/a |

| Overall Surplus for Year (Deficit) | n/a | n/a | n/a |

| Gard Group balance sheet summary | |||

| Balance Sheet | |||

| Net Assets | 2,211,503 | 2,255,363 | 2,287,205 |

| Net Outstanding Claims | 1,250,883 | 1,245,249 | 1,152,343 |

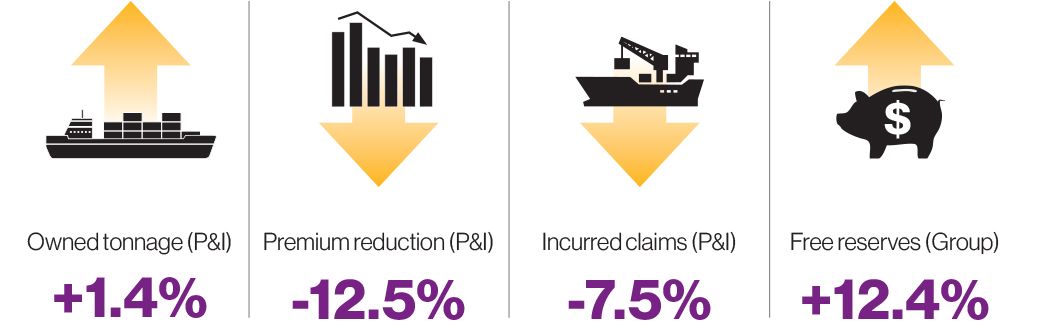

| Free Reserves | 960,620 | 1,010,114 | 1,134,862 |

| Entered tonnage (GT, millions) | 2015 | 2016 | 2017 |

|---|---|---|---|

| Owned/Mutual | 189 | 199 | 200 |

| Owned/Fixed | 19 | 16 | 17 |

| Chartered/Fixed | 58 | 90 | 90 |

| Total | 265 | 305 | 306.6 |

| (MOU: Mobile offshore units) | |||

| S&P Rating History | 2015 | 2016 | 2017 |

| A+* | A+* | A+* | |

| Average Expense Ratio (AER) | 2015 | 2016 | 2017 |

| Five years ending 20 February | 11 | 12 | 12 |

Combined ratios provide a direct comparison of club underwriting performance. The combined ratio is essentially the net loss ratio for the club and is defined as follows:

Combined ratio = |

(Net incurred claims + operating expenses) |

|---|

Gard changed their basis of reporting the P&I class of cover in 2010/11. Gard P&I underwriting results continue to be partially provided, but the club has progressively reduced the amount of information disclosed.

Since 2014/15 Gard has only published the combined Gard Group results for net paid claims, net change in the provision for claims, investment return, assets and free reserves (i.e. the combined results for P&I, Marine and Energy). In the table above we show the Gard P&I class underwriting results to the fullest extent disclosed. We therefore use Gard ‘Group’ figures for investment income, assets and free reserves.

To provide a meaningful comparison, the figures used in the financial graphs opposite represent Willis analysts’ estimates of solely the P&I proportion Gard’s investment income, assets and free reserves.