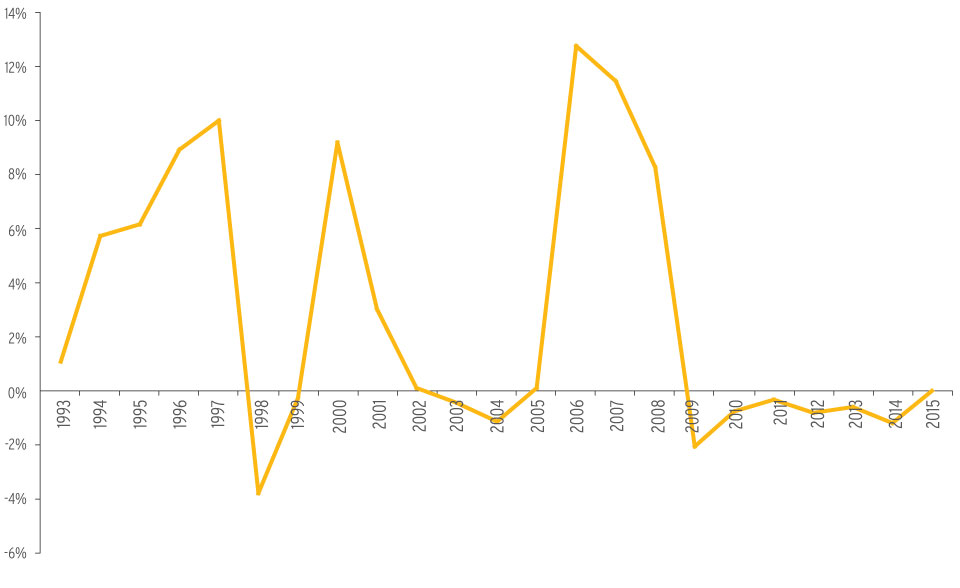

Following over 20 years of volatile financial performance, the P&I mutual market has experienced a period of relative calm over the most recent 6 years. The trend of the P&I market's deferred premium performance is outlined in the 'Market Average' graph below.

This graph shows the average deferred call accuracy of the whole market from 1993 to 2015. The main clubs over-calling in the mid 1990's were the Liverpool and London, Newcastle and Ocean Marine. These clubs were all subsequently forced to cease underwriting, either by merging or entering run-off. Since then there was a small peak of unbudgeted calls in 2001 when comparatively minor investment losses forced the Skuld and Steamship to over-call. The West of England made an isolated 'solvency' call in 2006 and the American Club has periodically called above their original budget. The most recent phase of widespread unbudgeted premiums was in 2008. The principal driver in 2008, if not the sole underlying cause, was enormous investment losses following the global financial crisis in that year.

It is noteworthy that over the last 6 years three clubs have, on average, been able to charge less than their full originally budgeted deferred calls (Britannia, Gard and UK P&I Club). Gard reduced their deferred calls in six consecutive years from 2009/10 to 2014/15. Britannia reduced their deferred call in 2009/10 and 2014/15; and the UK P&I Club agreed a 2.5% return in 2011/12 and 2014/15.

This is a measure whereby the clubs' deferred call performance can be directly compared. It provides a clear comparison, as individual clubs use a wide range of original estimate deferred calls.

Market average variance in estimated total call