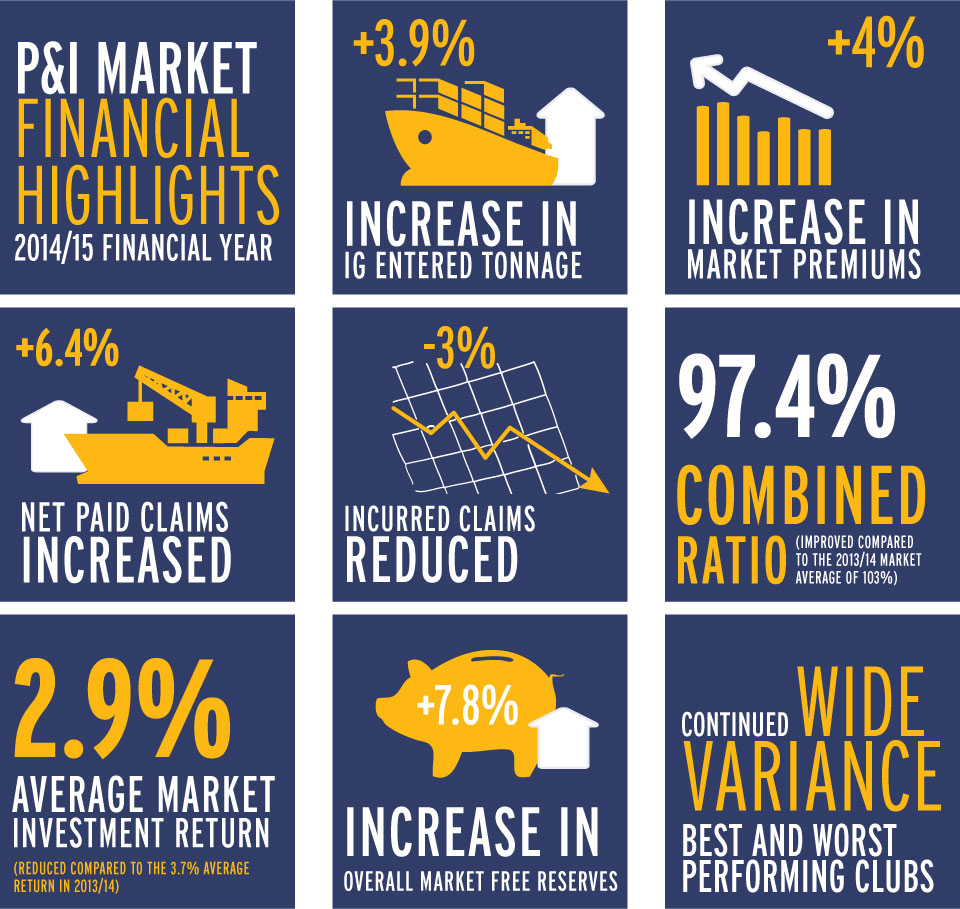

Financially, the International Group (IG) market is in the healthiest state in its history. All clubs which are subject to the capital requirement provisions of Solvency 2 are likely to satisfy these measures on implementation in 2016. Claims remain volatile and investment markets fragile, but a relative slowdown in number of major claims has allowed the IG market to make its first overall underwriting surplus since 2010.

The financial picture is not without its challenges however, a reversal of the current low incidence of major claims is entirely possible and there is no expectation for meaningful investment returns (if any) in 2015/16. The renewal in 2016 will similarly be contentious with the system of general increases creaking under the pressure of positive underwriting results and ship operators that need to reduce costs in any way possible.

In the context of the current financial position of the market clubs will find it increasingly difficult to persuade the 'many' that their premiums need to increase even if their own records are good and consequently competition is expected to be fierce. This renewal environment will add particular pressure on those clubs whose financial strength is below the average for the market.

The following comments relate to the combined financial year results of the individual clubs in the International Group. The only club excluded from this analysis is the Swedish Club, which reports on a basis materially different from the rest of the market. As the Swedish Club represents less than 2.5% of the IG P&I market, its omission does not affect the overall analysis materially.